IR BLOG

January-June 2025 results - Q&A

Sampo Group continued its excellent financial performance in the first half of 2025, driven by sustained top-line growth, particularly in Group’s target growth areas, and strong underwriting performance in a favourable claims environment.

The underwriting result grew by 25 per cent on a currency adjusted basis, contributing to a 16 per cent increase in operating EPS. Meanwhile, the Group combined ratio improved to 83.6 per cent (85.8), keeping performance well aligned with the financial targets.

The Group’s top-line development continued to be supported by strong momentum in the private business, both in the Nordics and in the UK. In Private Nordic, growth was driven by pricing, improving retention and increasing volumes, particularly in personal insurance. In Private UK, continued policy growth in selective areas, such as telematics, bike, and van insurance, as well as in home supported the top-line development.

Overall, the first half was characterised by a favourable claims environment, as the Nordics saw benign weather conditions, particularly in the first quarter. Benign weather, combined with large claims outcome being better than budget, led to a favourable claims experience that made the biggest impact on underwriting result compared to prior year.

After a strong second quarter, Sampo has decided to modestly adjust its outlook for the year. The outlook for 2025 underwriting result has been increased to 1,425–1,525 million (from EUR 1,400–1,500 million), representing growth of 8–16 per cent year-on-year. In addition, the outlook for 2025 insurance revenue has been raised to EUR 8.9–9.1 billion (from EUR 8.8–9.1 billion), representing growth of 6–9 per cent year-on-year.

| Key figures, EURm | 4-6/2025 | 4-6/2024 | Change, % | 1-6/2025 |

1-6/2024 |

Change, % |

|---|---|---|---|---|---|---|

| Gross written premiums | 2,542 | 2,333 | 9 | 6,242 | 5,631 | 11 |

| Insurance revenue, net | 2,264 | 2,057 | 10 | 4,452 | 4,077 | 9 |

| Underwriting result | 393 | 321 | 23 | 729 | 580 | 26 |

| Net financial result | 185 | 180 | 3 | 287 | 445 | -36 |

| Profit before taxes | 526 | 444 | 18 | 903 | 909 | -1 |

| Net profit | 417 | 310 | 35 | 703 | 653 | 8 |

| Operating result | 368 | 296 | 24 | 665 | 549 | 21 |

| Earnings per share (EUR) | 0.16 | 0.12 | 26 | 0.26 | 0.26 | - |

| Operating EPS (EUR) | 0.14 | 0.12 | 16 | 0.25 | 0.22 | 13 |

| 4-6/2025 | 4-6/2024 | Change | 1-6/2025 |

1-6/2024 |

Change |

|

| Risk ratio, % | 56.8 | 58.9 | -2.1 | 57.8 | 60.6 | -2.8 |

| Cost ratio, % | 25.9 | 25.6 | 0.3 | 25.8 | 25.1 | 0.7 |

| Combined ratio, % | 82.6 | 84.4 | -1.8 | 83.6 | 85.8 | -2.1 |

| Solvency II ratio (incl. dividend accrual), % | - | - | - | 174 | 179 | -5 |

Gross written premiums and insurance revenue include broker revenues. Like-for-like GWP growth is calculated by using constant currency rates and it is adjusted to exclude potential technical items affecting comparability, such as portfolio transfers, changes in inception dates for large contracts, and changes in accounting methods. Net profit for the comparison period refers to Net profit for the equity holders. Per share figures for the comparison period are adjusted for the share split in February 2025. The figures have not been audited.

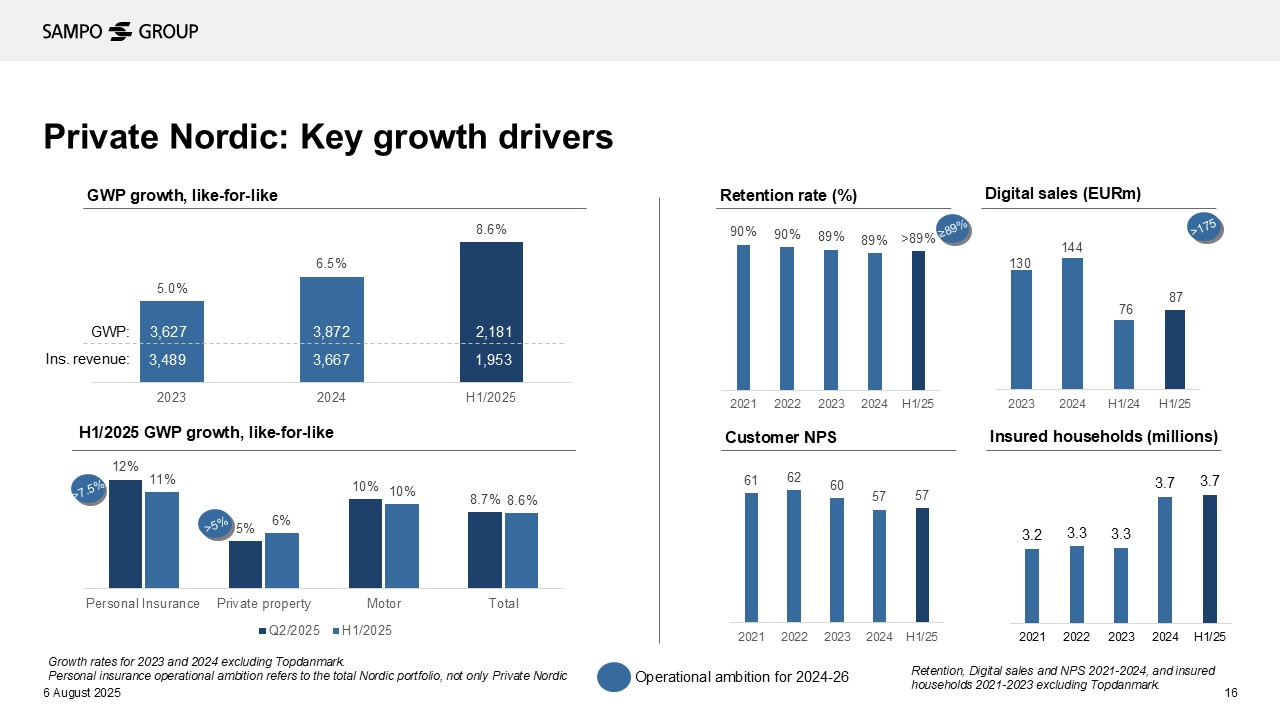

Private Nordic reported another quarter of very strong top-line growth on like-for-like basis. What were the main growth drivers?

The growth drivers have remained unchanged, with GWP supported by pricing, improving retention and an increase in volumes. In Q2, GWP growth on like-for-like basis was over 5 per cent in all major products, with personal insurance at 12 per cent and motor at 10 per cent. In addition, both the number of customers and the number of insured objects saw growth in Q2. As said, growth is broadly based across geographies and products, but the strongest momentum was in Norway, where we continued to benefit from supportive market conditions.

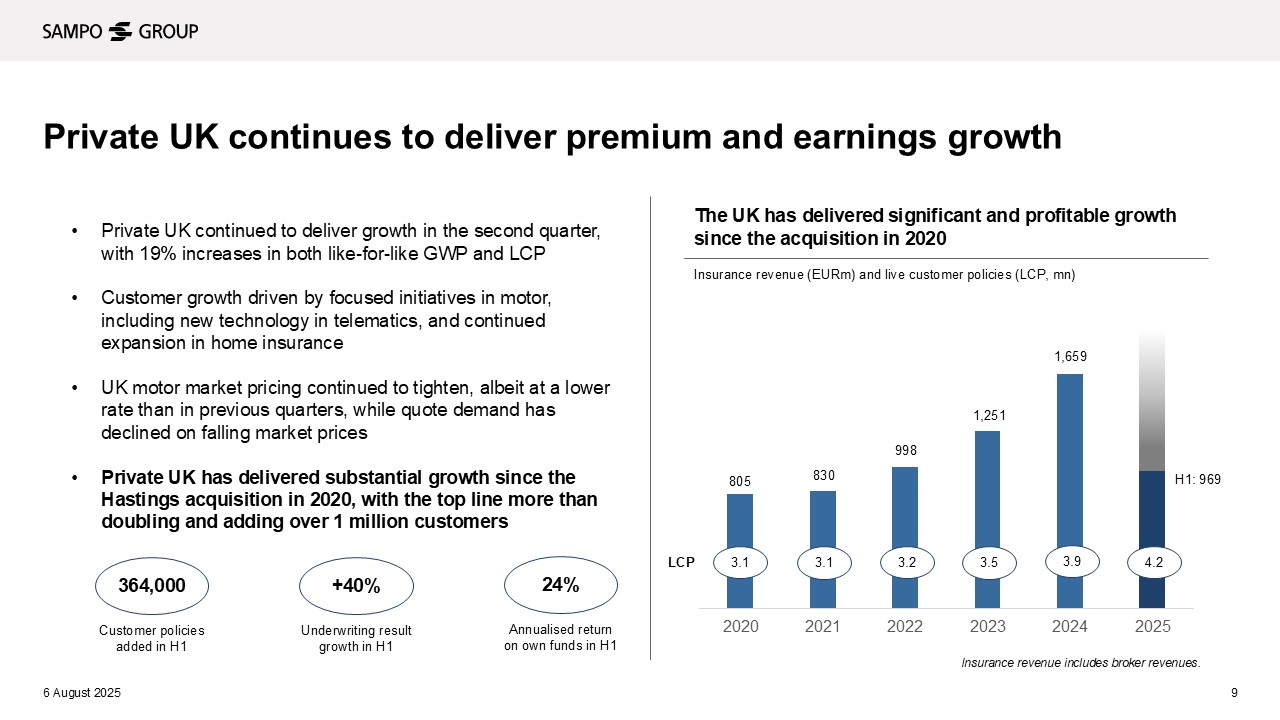

Private UK continued its solid top-line growth, albeit at a slower pace in Q2 compared to Q1. What were the key drivers behind this?

In Q2, premiums grew by 13 per cent year-on-year, 154,000 policies were added and underwriting profits increased by 22 per cent in the UK.

However, market-level price adequacy in the UK motor market is clearly lower than at the start of the year and compared to the prior year, although pricing stabilised during Q2. The decline in market prices has led to reduced activity on price comparison websites, which has supported higher customer retention but led to less new business opportunities to capture in the market.

In Nordic Industrial, GWP declined -6.6 per cent on like-for-like basis in Q2. Why is that?

In Industrial, our focus has been on securing the quality of our portfolio and managing the risk related to large property exposures. As we have communicated, we initiated de-risking actions in mid-2024 which have led to some loss of volume. These are now largely implemented, but the impact on volumes is expected to continue throughout 2025 and slightly in 2026 as well.

In the second quarter, the loss of volume was mainly related to a couple of larger property clients in Finland and Sweden, while Norway and Denmark saw broadly stable top-line development.

What were the key drivers behind the 21 percent underwriting result growth on a currency adjusted basis in Q2?

The underwriting result was supported by continued strong top-line growth and positive underlying trends, but the biggest impact compared to prior year came from favourable claims environment both in terms of weather conditions and large claims outcome. Severe weather and large claims had a positive effect of 1.9 percentage points on the Nordic risk ratio, whereas the comparison period saw a negative effect of 3.5 percentage points, primarily driven by large claims. However, the benefit from the favourable claims experience was partly offset by our prudent approach to reserving.

How did claims inflation develop in Sampo’s core markets?

In the Nordics, claims inflation remained stable at around 4 per cent. In the UK, claims inflation continued to moderate and has fallen back into the long-term range of mid-single digit percent.

Sampo raised again its underwriting result outlook for 2025. What explains the change?

The increase in the UW result outlook was driven mainly by the benign large and weather claims experience that we saw in Q1 continued into Q2. At the same time, the Group’s operational performance has continued to be excellent. As a result, we decided to modestly adjust the outlook for 2025.

Sampo’s performance has been running ahead of its targets, particularly in the UK. Have the targets been too conservative?

It is true that with the operating EPS growth of 13 per cent both in 2024 and in the first half of 2025 we are beating the target of more than 7 per cent annually on average for 2024-2026. However, regarding the target, the emphasis is on the term “more than”.

In the UK, our operational ambition is to achieve 10-15 per cent underwriting result growth annually on average during the strategic period. This was based on our somewhat conservative expectations for the next 3 years and a lot of positive things have happened since the beginning of 2024 when the ambition was set. Naturally, we are happy with the development in the UK so far.