IR BLOG

January–March 2026 results – Q&A

Sampo Group started 2026 with solid operating performance, backed by healthy growth in Nordic private and SME lines, strong margins across the segments, and a favourable claims experience despite a wintry start of the year.

The Group’s underwriting result grew by 9 per cent on a currency adjusted basis to 368 million (336) in January-March 2026 as a result of a materially better claims outcome than initially expected and attractive top-line growth through Nordic private and SME lines.

Driven by the stronger underwriting result but also supported by technical effects related to currency hedging, operating EPS increased by 19 per cent to EUR 0.13 (0.11). By contrast, reported EPS declined to EUR -0.02 (0.11), reflecting adverse investment returns driven by increased capital market volatility following heightened geopolitical tensions in the Middle East.

The Group’s combined ratio stood strong and improved to 84.4 per cent (84.6), benefiting from continued improvements in cost-efficiency and positive underlying trends in the Nordics, as well as a materially favourable large claims outcome.

After the strong start to the year, we have decided to increase the Group’s underwriting profit outlook for 2026 to EUR 1,525-1,625 million from EUR 1,485-1,600 million, representing growth of 3-9 per cent year-on-year. In addition, the outlook for 2026 insurance revenue has been adjusted to EUR 9.6–9.8 billion from EUR 9.5–9.8 billion, implying growth of 6–8 per cent year-on-year.

Given our strong balance sheet, we will launch a new share buyback programme of EUR 350 million based on our operating result for 2025 and the recent sale of NOBA shares.

| Key figures, EURm | 1-3/2026 | 1-3/2025 | Change, % |

|---|---|---|---|

| Gross written premiums | 3,752 | 3,701 | 1 |

| Insurance revenue, net | 2,363 | 2,188 | 8 |

| Underwriting result | 368 | 336 | 10 |

| Net financial result | -276 | 101 | – |

| Profit before taxes | 28 | 377 | -93 |

| Net profit | -46 | 285 | – |

| Operating result | 347 | 297 | 17 |

| Earnings per share (EUR) | -0.02 | 0.11 | – |

| Operating EPS (EUR) | 0.13 | 0.11 | 19 |

| 1-3/2026 | 1-3/2025 | Change | |

| Risk ratio, % | 59.6 | 58.9 | 0.6 |

| Cost ratio, % | 24.8 | 25.7 | -0.9 |

| Combined ratio, % | 84.4 | 84.6 | -0.2 |

| Solvency II ratio (incl. distribution accrual), % | 174 | 180 | -6 |

Gross written premiums (GWP) and insurance revenue include broker revenues. The GWP figure for January-March 2025 was restated in connection with the January-June 2025 result. Like-for-like GWP growth is calculated by using constant currency rates and it is adjusted to exclude potential technical items affecting comparability, such as portfolio transfers, changes in inception dates for large contracts, and changes in accounting methods. The figures in this report have not been audited.

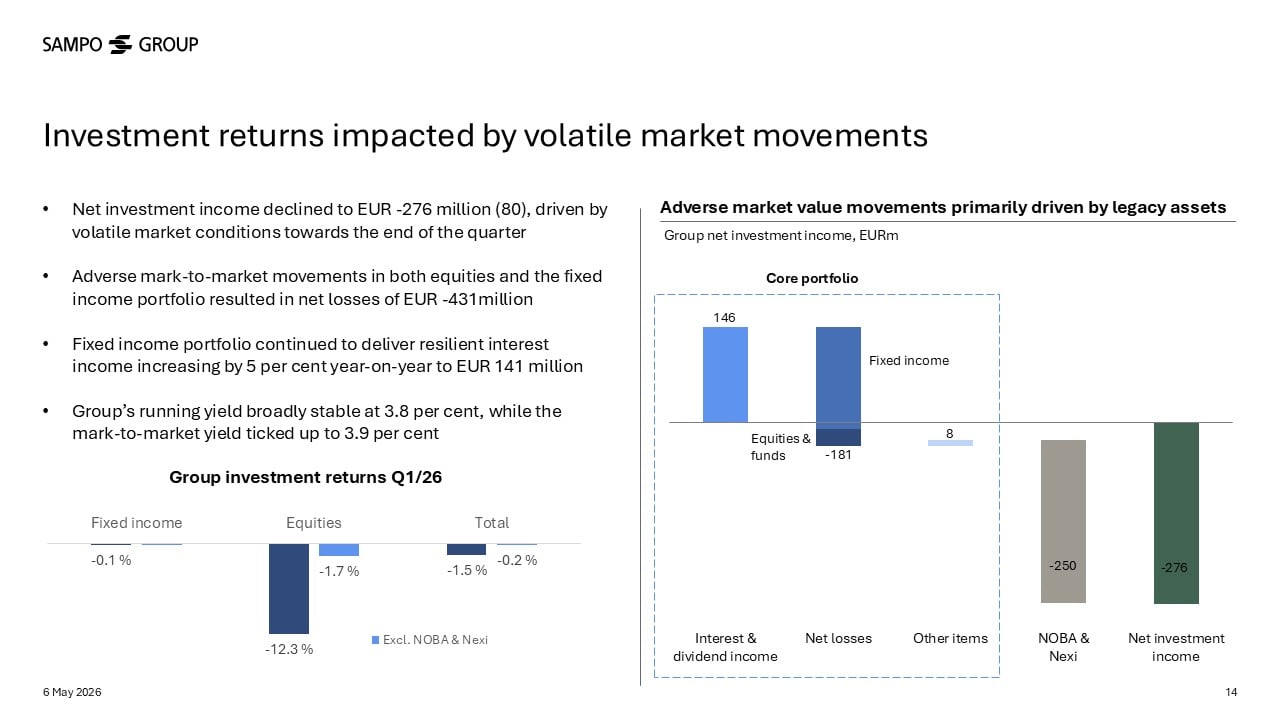

The Group’s net profit turned negative in the first quarter. How should investors read this?

The key takeaway is that the Group’s operating performance remained strong, while elevated capital market volatility dragged the investment result into negative territory, resulting in a negative net profit of EUR -46 million. In total, net losses from equities amounted to EUR -247 million and from fixed income portfolio to EUR -156 million. Despite this, the Group’s balance sheet remained robust.

As shown on the following slide, the Group’s core investment portfolio remained broadly stable, while net losses from equities were primarily driven by legacy assets, particularly NOBA. Excluding the legacy assets, namely NOBA and Nexi, the Group’s total investment return in the first quarter would have been -0.2 per cent, compared with -1.5 per cent as reported.

Quarterly volatility is a natural part of investing. The Group’s long-term average investment returns of 4.1 per cent over 2009–2025 reflect the effectiveness of our investment strategy.

Private Nordic reported another quarter of robust top-line growth. What were the key drivers behind the 6 per cent like-for-like GWP growth?

In Private Nordic, the high-quality growth seen in 2025 continued into the first quarter driven by solid new sales, high customer retention, and positive portfolio development. Growth was driven by continued positive development in key target areas. Personal insurance continued to deliver strong growth, increasing by 9 per cent, while motor grew by 5 per cent, and private property by 4 per cent.

Momentum in digital sales remained strong with growth of 14 per cent, underpinned by positive development in insured objects, particularly in Finland and Denmark, demonstrating the Group’s strong digital capabilities across markets. While Finland is the most digitalised P&C market in the Nordics, followed by Sweden and Norway, digital adoption in Denmark remains lower than in other Nordic markets, providing an attractive opportunity to drive growth by leveraging our digital capabilities and scale following the Topdanmark acquisition.

Growth in UK Private continued to moderate with like-for-like GWP growth at 1 per cent. What drove the performance?

In the first quarter of 2026, we continued to find pockets of growth, leading to 3 per cent growth in live customer policies (LCP) quarter on quarter, supported by higher retention and increased sales in higher premium products such as telematics. During the same period, like-for-like GWP growth came in below LCP growth, reflecting a softer pricing environment.

While the UK motor market has seen emerging price stabilisation recently, the market remains competitive and our growth appetite highly selective, as reflected in volumes.

We continue to focus on underwriting discipline and portfolio quality that will ensure that we are well positioned to capture attractive growth opportunities once the market turns. Meanwhile, we continue to invest in our capabilities that support our long-term growth ambitions.

What were the key highlights of Nordic Commercial and Nordic Industrial?

Our Nordic SME business continued to deliver healthy growth driven by high retention, increasing customer numbers, and solid development in digital sales. In total, we gained more than 2,300 new customers over the quarter, with digital sales up 9 per cent year on year.

This was partly offset by softer competitive landscape on the large corporate side, affecting Nordic Industrial and the larger end of Nordic Commercial. On the other hand, we benefited from lower reinsurance prices, supported by favourable market conditions and earlier actions taken to reduce large property exposures. As a result, like-for-like GWP growth in Nordic Commercial came in at 1 per cent. Nordic Industrial delivered a like-for-like GWP decline of

-1 per cent, with volumes remaining broadly flat following competitive 1 January renewals and continued pressure on repricing levels. In Industrial, we focus on ensuring high and stable profitability.

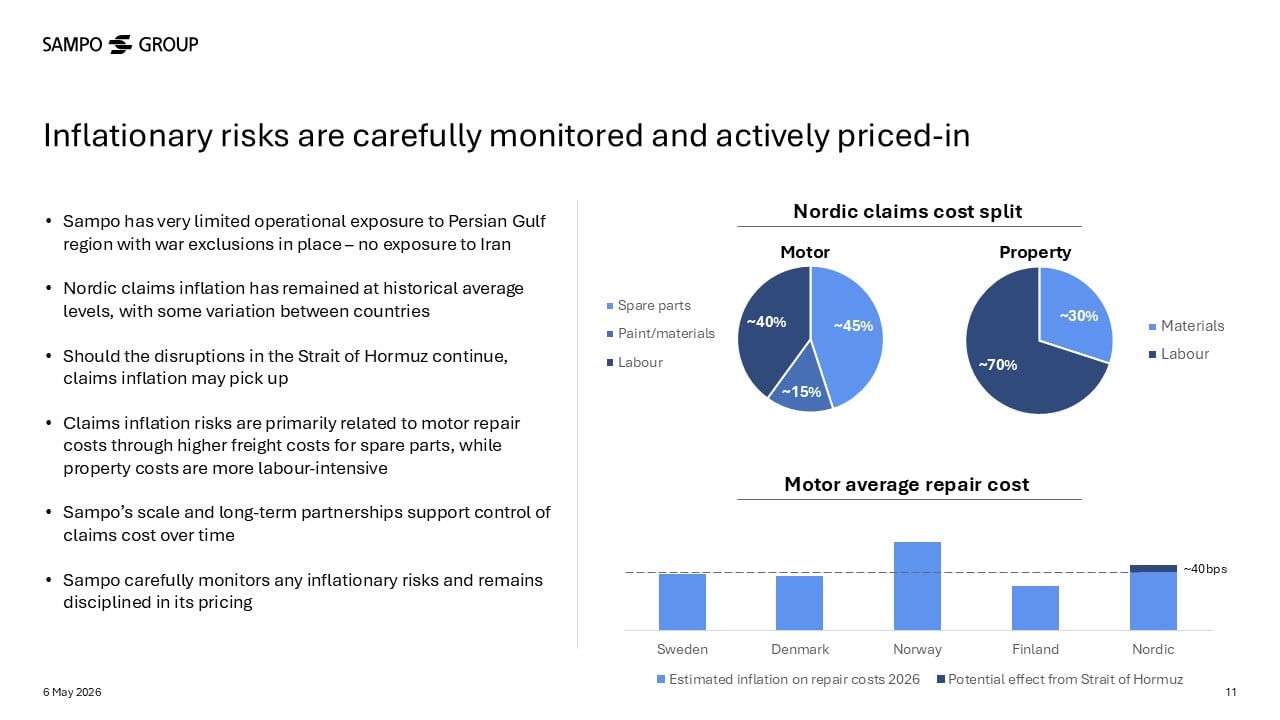

What impact could disruptions in the Strait of Hormuz have on claims inflation?

As always, we are monitoring claims inflation closely and maintain a disciplined approach to pricing. If disruptions in the Strait of Hormuz continue for a prolonged period, there is likely to be upward pressure on claims inflation. For Sampo, spillover effects are mainly linked to motor repair costs due to higher freight costs for spare parts. Property costs are more labour-intensive and less exposed to material price movements.

Overall, the Group’s scale and long-term partnerships give us good visibility on costs and support disciplined cost management over time, as we showed during the 2022–2023 inflation spike, which we managed well.

What is the status regarding Topdanmark synergies?

The integration is going well, with cost synergies emerging faster than we have planned. Following strong delivery in 2025, we have reassessed the phasing of synergies. As a result, the run-rate synergy has been increased to EUR 105 million for 2026 and to EUR 125 million for 2027 from EUR 55 million and EUR 87 million, respectively, while we stick to our EUR 140 million synergy target for 2028. By the end of March 2026, EUR 58 million of the targeted run-rate synergies had been realised.

Autonomous vehicles (AVs) have been a hot topic recently. How will AVs affect the risk pool in motor insurance?

Frequencies of collisions and some other claims may decrease with the adoption of AV technology over time, but cars becoming safer is a trend that has continued for decades. As an insurer, we are excited about increasing customer safety through advanced car technology.

However, while frequencies may decrease, the risk pool is expected to increase as a result of higher severity. Cars full of technology are more expensive to repair and they need to be repaired properly throughout the lifecycle of the car, translating to longer need for Casco insurance. In the Nordics, motor insurance has become more of a service product as a result of this, and we believe this trend will continue. AVs may also increase total miles driven across the car fleet by unlocking previously unserved demand for personal car travel.

Complex technology and wide variation in repair costs between different car brands and models favour big insurers with comprehensive data lakes and insight through OEM partnerships.

We believe that the rapid increase in advanced car technology provides compelling opportunities for Sampo, enabled by our scale, comprehensive diversification and market-leading partnership network with OEMs.

What are the implications of the Danish Supreme Court ruling for Sampo?

In summary, the Danish Supreme Court ruling means that the applied compensation threshold for permanent loss of earning capacity in workers’ compensation cases will be retrospectively lowered from 15 per cent to 5 per cent.

This is an adverse outcome for both the Danish insurance industry and the State and municipalities in Denmark, as it will have financial consequences. Sampo, in line with the Danish insurance industry, expects the State of Denmark to take responsibility for the industry’s losses.

Sampo has established a number of scenarios and will continue to analyse the ruling. Based on current best estimates, the potential impact is expected to be covered by Sampo’s existing reserves, thanks to our disciplined reserving practices. Therefore, the effects on Sampo’s net profit and solvency are expected to be limited.