IR BLOG

January-March 2021 results – Q&A

Sampo’s first quarter of 2021 was very strong across the Group. Profit before taxes amounted to EUR 632 million (162) and earnings per share was EUR 0.82 (0.26). It was the best-ever Q1 in the Group’s history, if the sale of Sampo Bank in 2007 is not taken into account.

Sampo’s core business, P&C insurance, reported its best-ever operational results. The Group’s underwriting profit was EUR 317 million and combined ratio 81.2 per cent.

Sampo’s largest subsidiary, If reported a profit before taxes of EUR 257 million (129) and an underwriting profit of EUR 213 million (180). If’s combined ratio improved to 81.5 per cent (83.7). Following the strong performance in the first quarter, If’s combined ratio outlook for 2021 improved to 82 – 84 per cent from below 85 per cent.

| Key figures, EURm | 1-3/2021 | 1-3/2020 | Change, % |

|---|---|---|---|

| Profit before taxes | 632 | 162 | 290 |

| If | 257 | 129 | 99 |

| Topdanmark | 137 | -13 | - |

| Hastings | 46 | - | - |

| Associates | 126 | 86 | 47 |

| Mandatum | 76 | -16 | - |

| Holding (excl. associates) | -11 | -24 | -54 |

| Profit for the period | 526 | 139 | 278 |

| Key figures | 1-3/2021 | 1-3/2020 | Change |

| Earnings per share, EUR | 0.82 | 0.26 | 0.56 |

| EPS (incl. change in FVR), EUR | 1.39 | -1.71 | 3.10 |

| NAV per share, EUR* | 23.28 | 19.82 | 3.46 |

| Average number of staff, FTE | 13,204 | 10,303 | 2,901 |

| Group solvency ratio, %* | 189 | 179 | 13 |

| RoE, % | 26.0 | -33.2 | 59.2 |

*) Comparison figures of 31 December 2020.

The figures have not been audited.

How did the coronavirus pandemic affect If’s business in the first quarter?

The pandemic continued to lower the claims frequency, which decreased claims costs especially in motor and travel insurance. The effect of the pandemic on If’s risk ratio was approximately 3 percentage points positive in the first quarter.

In terms of premium income, the sale of travel insurances decreased significantly due to the pandemic. In addition, the premium effect in the corporate segments was noticeable and mainly related to workers’ compensation insurance in Finland. For If as a whole, the pandemic had not a significant effect on premium volume.

What were the drivers behind If’s strong results in the first quarter?

The result was partly supported by lower claims costs due to the pandemic and partly by investment income boosted by a good momentum in the markets, but even without these factors, If’s performance was strong. This is the result of If’s continuous and determined improvements of operational efficiency and investments in digitalization.

Combined ratio was 81.5 per cent. Without the approximately 3 per cent positive COVID-19 effect, it would have been 84.5 per cent, which is an excellent performance in the quite wintry first quarter.

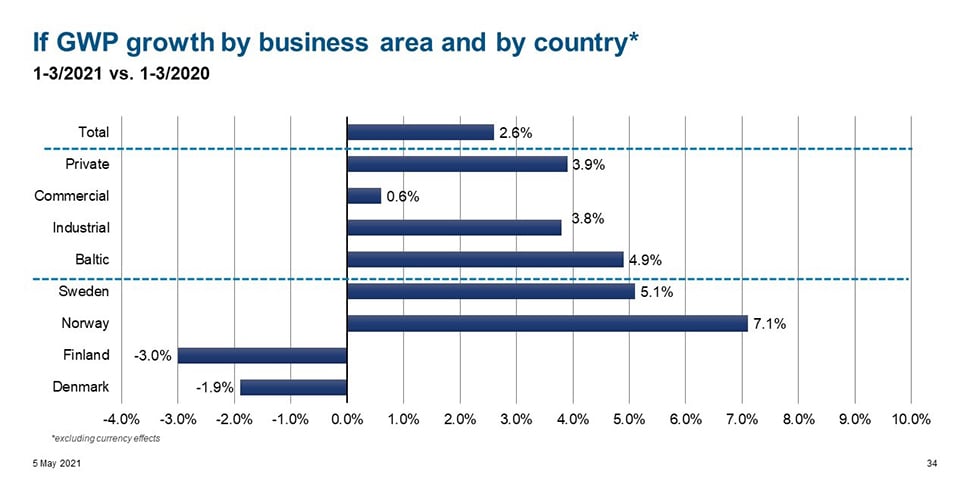

If’s premiums grew 2.6 per cent in local currency in the first quarter. What were the drivers behind that?

The main driver was the strong 3.9 per cent growth in BA Private, If’s largest business area. One of the factors supporting the growth in BA Private was the increased new cars sales, in which If is the leading insurer supported by its strong partnership network.

In addition, the first quarter is important for corporate segments since large part of insurance contracts are renewed on the first day of the year. The premium growth within corporate segments was characterized by stable retention and selective rate actions.

Picture from Supplementary Financial Information presentation

Why did the premium decrease by 3.0 per cent in Finland?

In Finland, the coronavirus pandemic had a negative effect on volume of workers’ compensation insurances as wages decreased due to lower economic activity.

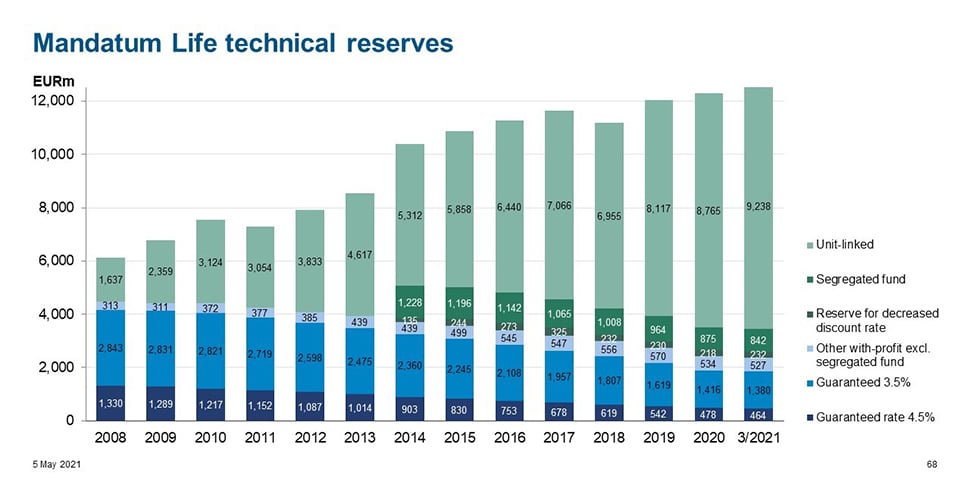

What were the drivers behind Mandatum’s strong results?

Of Sampo’s businesses, the development in the equity and fixed income markets affect Mandatum the most, since vast majority of its results comes from investment income. In addition to the general market development, Mandatum’s results were supported by a quite large capital gain related to the takeover bid for Tikkurila.

Mandatum’s profit before taxes was very strong, EUR 76 million, despite the fact that the profit included a negative impact of EUR 31 million from lowering the discount rate for 2024 to 1.5 per cent.

Mandatum Life’s unit-linked technical reserves were supported by the good momentum in the markets and increased to a new record of EUR 9.24 billion.

Picture from Supplementary Financial Information presentation

How did Hastings first full quarter as a part of Sampo Group go?

Hastings reported strong results in a somewhat challenging market environment. In the UK, the coronavirus pandemic pushed the claims frequency down, but at the same time, average premiums decreased, and price competition increased.

Hastings has taken a disciplined approach and did not participate the aggressive price competition, keeping its number of live customer policies and market share stable at year-end 2020 level. Hastings’ profit before taxes amounted to EUR 46 million, including EUR 10 million charge for amortization of non-operational intangibles, which will continue for the next seven years.

Hastings operating ratio was very strong, 75.1 per cent. The ratio includes a 3.4 percentage points benefit from acquisition accounting across revenue and operating expenses for deferred acquisition costs and other fair value adjustments that will continue until the end of 2021.

Picture from Supplementary Financial Information presentation

How did Sampo’s solvency and financial leverage develop in the first quarter?

Sampo Group’s Solvency II ratio was strong, 189 per cent at the end of March, well in line with the target range of 170 – 190 per cent for 2021 – 2023. Financial leverage was 28.0 per cent, in line with the target level of below 30 per cent for 2021 – 2023.

Sampo’s lock-up period for Nordea shares ends on 9 May 2021. When will Sampo continue to reduce its ownership in Nordea?

As we communicated at the Capital Markets Day in February, Sampo will materially reduce its ownership in Nordea over the next 18 months (approximately over 15 months at the time of writing this). The schedule of next actions depends on many things, of which the share price of Nordea is naturally the most important one.

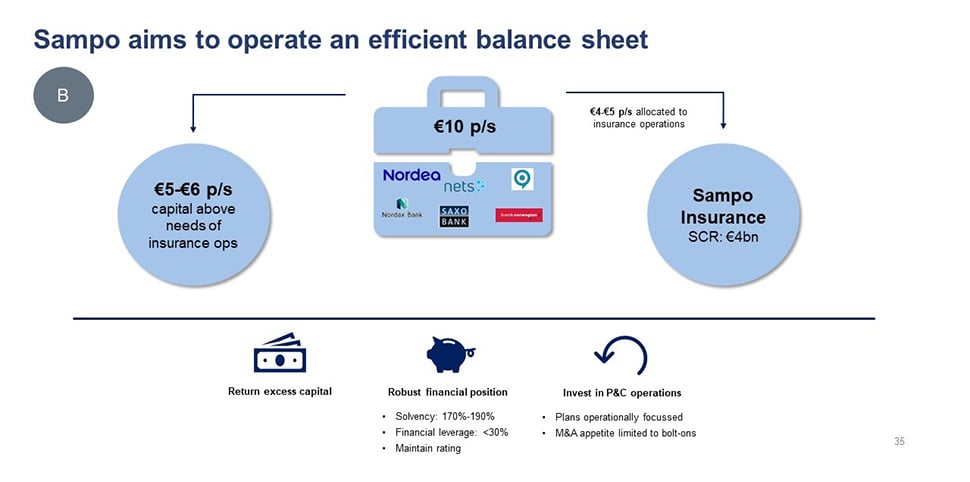

At the Capital Markets Day, Sampo estimated that after exiting Nordea and other financial investments it would have approximately EUR 5-6 per share excess capital. Is this estimate still valid?

That estimate presented at the Capital Markets Day was round and based on figures at the end of 2020. The biggest factor is the share price of Nordea, which was EUR 6.67 per share at the end of 2020. Favorable market development will naturally increase the amount of potential excess capital.

Picture from Capital Markets Day presentation (24 February 2021)

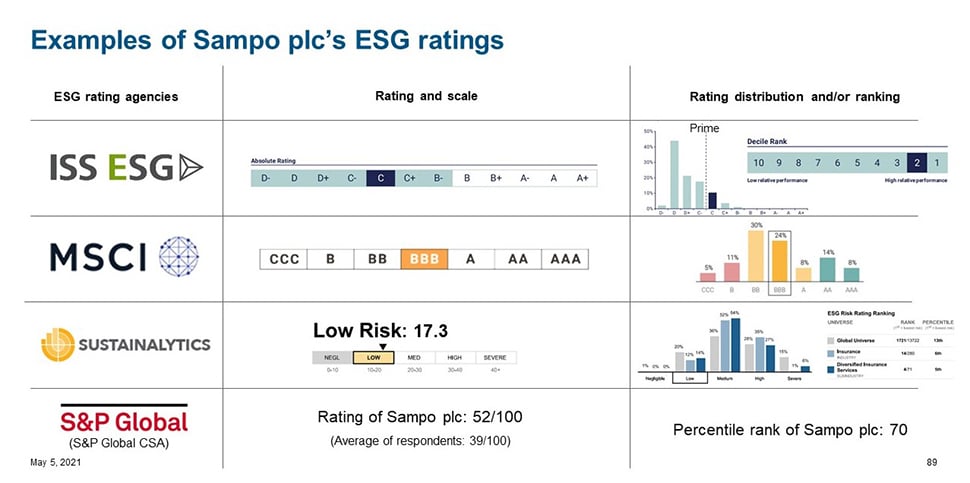

Sustainalytics, an ESG-focused research company, upgraded Sampo to Low Risk. What does this mean?

The rating change made by Sustainalytics proves that our continuous and determined work on corporate responsibility bears fruit. Sampo is now in the top five of the 71 insurers rated by Sustainalytics and the number one with a market cap of EUR 20 – 40 billion. We are pleased with this achievement but there is still room to further improve and the work on that field continues.

Picture from Supplementary Financial Information presentation

What would you like to ask Sampo’s managers?

Sampo will hold a Q&A session in connection with its Annual General Meeting on 19.5. In the Q&A session, the Group CEO Torbjörn Magnusson and Group CFO Knut Arne Alsaker will answer shareholders questions. Questions can be presented during the live event, but we would like to receive those in advance as well.

Questions can be sent by email to ir@sampo.fi.