IR BLOG

Sampo is an opportunistic and patient investor

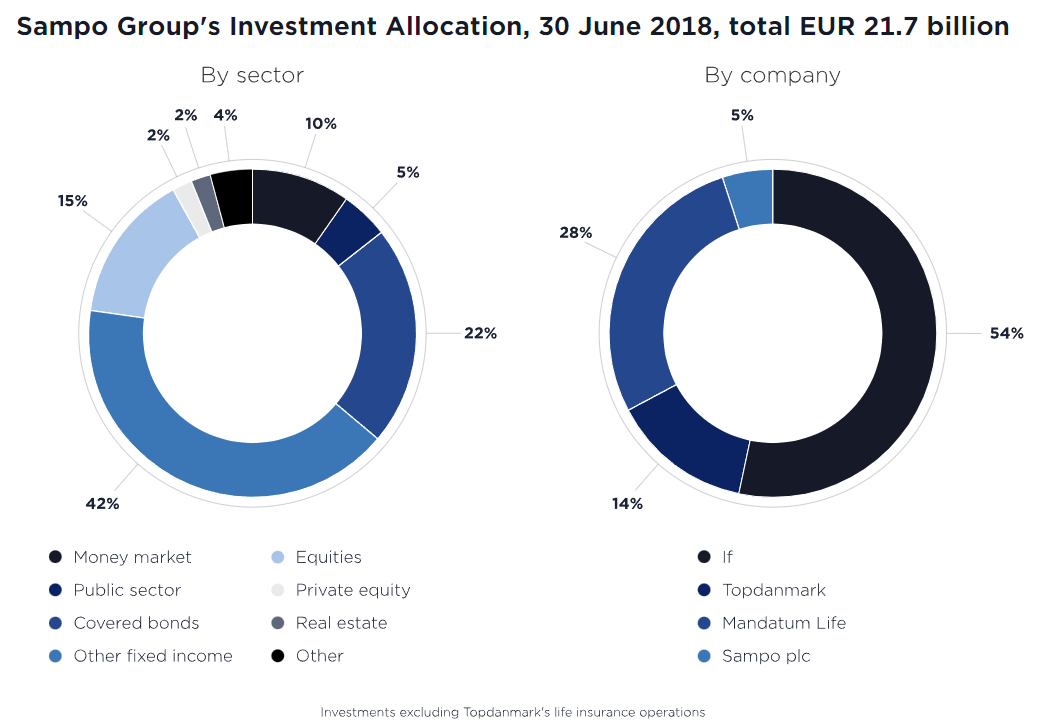

Sampo Group is the largest player in the Nordic insurance sector. Not many people know that Sampo is also one of the largest investors in the region. At the end of June 2018, Sampo had investments worth near EUR 22 billion. Thus, we are in the same league as the large Finnish pension funds.

However, a big investment portfolio does not require a large battalion of portfolio managers. Vast majority of the Group's investments are managed by the team of six portfolio managers sitting at the Sampo headquarter at Fabianinkatu, Helsinki. In addition, there are six portfolio managers in If in Stockholm. Both teams report to the Chief Investment Officer Patrick Lapveteläinen.

Sampo's investment philosophy is to be an opportunistic long-term investor.

"We are patient, contrarian and we don't follow indices. Time to time, there occurs stupidity in the markets and we have both competence and liquidity to take advantage of them", says Ville Talasmäki, the Head of Allocation.

By stupidity Talasmäki refers especially to the herd behavior in the markets, which can lead strong movements in both directions.

"Many investors benchmark themselves to some index and invest at least partially like the index, because they fear to perform worse than the index. For many investors, the fear of being wrong alone is more powerful than the chance of being right alone."

"One good example of this behavior is the 100 year bond issued by Argentina last year. Argentina has defaulted several times, but many investors bought the debt just because it's part of certain emerging markets indices. Since the issuance, the bond price has gone down by 25 per cent."

Big size brings big benefits

The fact that Sampo is a big and globally well-known investor, brings great benefits. Because of that, vast amount of different investment ideas and opportunities to participate M&A deals are presented to us every year. Much of the portfolio managers job is to meet corporate executives and bankers.

Some of the ideas presented to us end up in Sampo's portfolio, but the majority of them gets denied. Talasmäki reminds that a stock or a bond of a good company is not automatically a good investment. In order to be a good investment, the price has to be right from the point of view of a long-term return potential. Sometimes, the right buying opportunity requires a lot of patience. Nordax and Intrum are good examples. We followed closely these companies for years until we saw that the time was right to push the buy button.

In addition to the long-term return potential, responsibility matters are also important. Sampo is currently adapting more systematic ways to take corporate responsibility into account when making investment decisions.

Sampo's individual investments are usually worth between EUR 10 and 100 million. In order to keep up-to-date on our investments, Sampo's portfolio managers usually meet each company's executives 2-4 times a year. In the case of a larger investment in a company that operates in the financial and insurance sector, Sampo aims to influence its operations via board positions. Saxo Bank and Asiakastieto are good examples for that.

Sampo has investments around the world. Investments in North Europe and especially in the Nordics are mainly managed internally, whereas in global investments we tend to use external mutual funds.

"When choosing an external fund manager, the most important criterion is that he or she brings added value and bold enough ideas. If we wanted just to follow some index, we could easily do that by ourselves using etf:s", says Talasmäki.

According to Talasmäki, one of the biggest benefits of Sampo's portfolio team are small boundaries between different asset classes.

"When we find an interesting company, we can very flexibly choose whether we want to invest in its debt or equity."

The current market situation is challenging for Sampo. Interest rates have been exceptionally low for years, thanks to central banks' monetary stimulus measures. Because of that, good returns from fixed income are difficult to find.

"Without taking duration or credit risks, it's really hard to get decent returns from fixed income. In the U.S. interest rates have been rising but our insurance operations' technical reserves are mainly in euros, which limits our ability to invest in dollar debt."

Even tough stock valuations are very high in many markets, stocks are currently the best asset class. In fact, Sampo has been overweighting stocks for a long time now. However, the importance of stock picking has become even more pivotal. Our largest equity investments are in the Nordic financial and insurance sector, which is our core competence area.