IR BLOG

Bond issue – Case Sampo’s EUR 1 billion bond

Companies generally use both equity and debt to finance their investments and operations in order to keep their capital structure optimal and return on equity attractive. Debt can be obtained directly from a bank in the form of a bank loan or from the financial markets by issuing bonds.

Due to regulatory and practical reasons, usually only institutional investors and private investors classified as professional investors can make orders for corporate bonds in the primary market. The minimum settlement amount is usually EUR 100,000.

This blog entry opens up the process behind the bond issuance with using Sampo’s EUR 1 billion Tier2 hybrid bond issued at the end of August to fund the Hastings acquisition offer as an example.

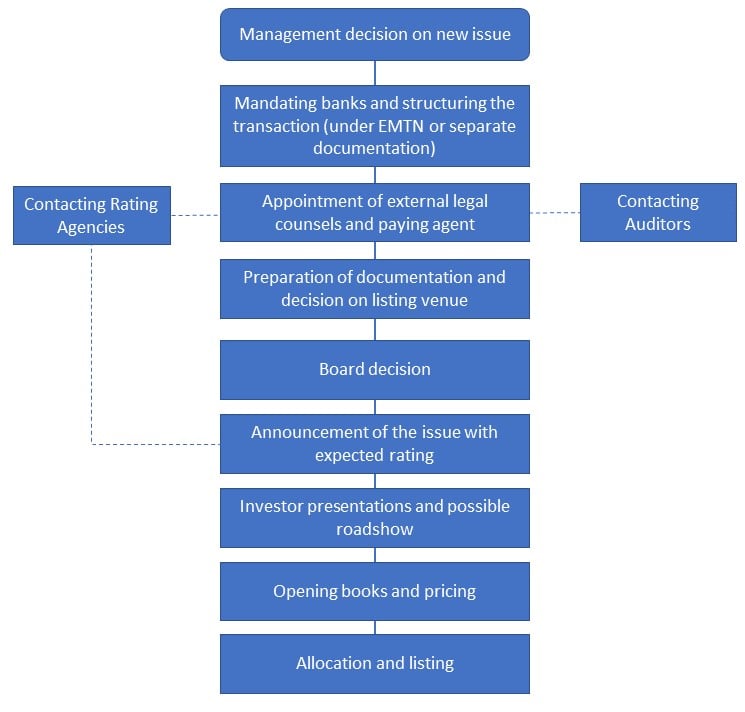

Decisions on financing, selecting the bookrunner banks for the issue and documentation

The management of the company makes the decision on raising debt capital from the financial markets, but the bond issue usually also requires a Board approval. The type of a bond that the company decides to issue depends on many factors, but the company’s current debt structure and the maturity profile of its bonds issued are key factors when deciding on the maturity of a new bond – and of course the interest rate levels.

From the balance sheet and cash management point of view, it is desirable that the maturity profile of the bonds is smooth over the coming years. The first call date for Sampo’s new EUR 1 billion hybrid bond is 12 years from the issue date, i.e. in 2032, which is currently the longest-maturity bond for Sampo.

Maturity profile of Sampo’s debt instruments prior the new issue (30 June 2020)

Once management has decided to issue a bond, the next step is to select the bookrunner banks for the issue and to start preparing the legal documentation required for the issue. The extent of the documentation process depends on whether the bond is issued under an existing bond program or under separate documentation. Sampo’s EUR 1 billion hybrid bond was issued under its existing EUR 4.5 billion EMTN (Euro Medium Term Note) program.

At this stage, the company is also typically in contact with the credit rating agencies, assuming the bond will be rated. Credit rating is a key factor for the spread level of the bond and determines what kind of investors will be interested in investing in the bond. Many investors require that the bond has at least an investment grade rating from the leading credit rating agencies (S&P/Fitch BBB- and Moody’s Baa3). In addition, some investors favor bonds that have a rating from two different agencies. Sampo’s hybrid bond has BBB+ rating from S&P and Baa1 rating from Moody’s.

Mapping investors’ interest

Once the documentation is completed and the expected ratings are confirmed, markets will be informed about the planned issuance. In practice, this means that the preliminary information about the bond will appear on Bloomberg screens or will be sent to investors in the form of a mandate announcement.

At the same time, the bookrunner banks begin marketing the bond and survey investors’ interest and preliminary thoughts on the spread level. The bookrunners usually have a good idea of the type of investors that might be interested in investing in the bond. Also, investors are often in direct contact with the bookrunners after seeing the preliminary details of the bond. These initial discussions with potential investors give an idea of the initial spread level and the size of the order book.

In case the company has not previously issued similar bonds or the company is less familiar to international investors, views on attractive spread levels may vary a lot. As Sampo is a well-known company in the market and issued a EUR 500 million hybrid bond in the Spring 2019, it was easier for the bookrunners to gather the feedback on pricing from investors. Comments on pricing may be quite general or very precise and are usually expressed as a credit spread to the reference rate (Euro Mid-Swap rate).

The feedback given by the investor could be, for example: “I’m interested, if the rate is MS + 270-280 basis points and I could invest EUR 20-30 million.”

Concurrently with the process of gathering feedback, meetings with the company’s management are arranged for the interested investors. During the pandemic, these meetings are held by telephone or via virtual events. In normal times, the company would also arrange roadshows in the major financial hubs. Prior to this year’s issue, Sampo held virtual roadshows with over 50 investors within two days.

Since fixed income investors have a somewhat different risk tolerance level compared with equity investors, their questions also differ from equity investors’ questions. Balance sheet, debt coverage and capital structure are usually the key factors for fixed income investors to focus on, whereas expectations on next year’s dividend does not raise that much attention.

‘Go’ or ‘No-go’ call

Once the investor roadshows are done and there’s a good view on the initial investor demand, the books are ready to be opened for investors’ orders. As orders are received in one day and the whole process takes only a few hours, the issue must be carefully planned and the prevailing market sentiment well-observed. However, sometimes, issuers are forced to move ahead with issuance even if the time is not optimal from their perspective.

When the Covid-19 crisis hit the market with full force in the spring, plummeting stocks filled the news headlines in financial media. However, less attention was paid to the fact that at the same time, credit spreads of corporate bonds shot up and the new issue market was totally stalled. For example, the credit spread of Sampo’s hybrid bond issued last year rose from below 200 basis points at the end of February to almost 400 basis points at its worst.

For a while, it was almost impossible for companies to issue new bonds. No investor really dared to make bids or if dared, the rate demands were very high. The general market sentiment can therefore significantly affect investors’ appetite and the required rate of return. When talking about bonds worth hundreds of millions or billions, even small movements in rates matter.

In the morning of the planned bond issue, the bookrunners have a so-called ‘Go’ or ‘No-go’ call with the issuer, during which final decision to open the books for the bond is made.

Opening the books and pricing process

When the books are opened for investors’ orders, the bookrunners announce the preliminary spread level based on the investor feedback. In the case of Sampo’s hybrid bond, the books opened on 27 August 2020 at 10:15 am with initial price talk of MS+300 basis points area.

The orders received during the first hours play an important role for the final pricing as attention generates more attention. For Sampo’s bond, there were orders worth over EUR 2 billion received during the first hour. After two hours, the price guidance was lowered to MS + 270 basis points (+/- 5) area. When the books are open, investors can withdraw their bids at any time. Thus, one must be very careful when setting the price guidance so that that investors will not lose their interest in the bond if the spread falls too low. At 1:55 pm, the book exceeded EUR 5 billion and was closed and the final spread was set at MS + 260 basis points. Over 350 investors participated in the issue and most orders were received from the UK/Ireland, German-speaking Europe and the Nordics.

The coupon rate of Sampo's hybrid bond maturing in September 2052 was set at 2.50 per cent, payable until 3 September 2032, which is the first date for the bond. If the bond is not redeemed at its first call date, the coupon rate will step up to 3m Euribor + 360 basis points until the final maturity.

Allocation and listing on the stock exchange

As the size of Sampo’s hybrid bond was EUR 1 billion and the book was 5 times oversubscribed, investors’ orders had to be scaled back. The allocation of the bond is decided by the company together with the bookrunners in accordance with pre-defined allocation principles.

In the event of an oversubscription, priority is normally given to investors who have given constructive feedback during the process, i.e. shown meaningful interest with preliminary orders at reasonable price level during the roadshow, which has helped the company and the bookrunners to form a better view on pricing as well as investors who were among the first to give their orders to the bookrunners when the books were opened.

Once the allocation is complete and trades are settled, the bond will be listed on a stock exchange. Sampo’s hybrid bond was listed on the London Stock Exchange on 3 September 2020.

Issuing new debt in Sampo